Article

Deloitte 2024 Q1 CFO Express

Issue No. 13

Published date: 16 April 2024

Explore Content

- Play this episode

- Establishing the new before destroying the old

- Interpretation of 2024 Government Work Report and Industry Outlook

- Q1 2024 Review and Outlook for Chinese Mainland & HK IPO markets

- The next set of imperatives for CFOs in the Asia-Pacific region, reveals Deloitte Survey

- A guide to emerging technologies for CFOs

- New frontiers of sustainability: Double Materiality explained

- 2024 Global Human Capital Trends: Embracing Human Sustainability

2024 is a crucial year for achieving the goals and tasks of the 14th Five-Year Plan. The economic growth target for this year is "around 5%", which is the same as the target for 2023. The complexity and uncertainty of the external environment still exist, but the logic of China's economic development is showing significant changes, gradually shifting from a growth model dependent on investment and exports to one driven by domestic demand and the development of new technologies and new quality productive forces. On the one hand, expanding domestic demand is a key measure for stabilizing growth. China is actively promoting new types of consumption while stabilizing traditional types of consumption, encouraging the replacement of old consumer products with new ones, and emphasizing the expansion and upgrade of consumption in livelihood services. On the other hand, through leveraging technological innovation, especially disruptive technological innovation, new industries, new models, and new business forms are being created to build new engines of growth for the Chinese economy and inject momentum into economic development.

This year's government report clearly states that "the unit energy consumption of GDP will decrease by about 2.5% in 2024", and the quantitative target for reducing energy consumption per unit of GDP is reiterated in the government work report, reflecting that green and low-carbon development remains an important direction for the Chinese economy. To further improve the standardization of Environmental, Social, and Governance (ESG) reports, the Shanghai, Shenzhen, and Beijing stock exchanges have simultaneously issued guidelines for the disclosure of sustainability information, and external pressure is driving companies to consider energy efficiency and improve their management levels related to climate change. Against this backdrop, the role of Finance is further expanded, and new technologies such as artificial intelligence and big data are rapidly empowering it.

- In response to the requirements of the disclosure of sustainability information, what preparations should companies make in terms of compliance and information disclosure? What impact will the challenge of double materiality assessment have on the work of the finance department?

- In the era of artificial intelligence, how should CFOs balance the potential value and risks of emerging technologies?

- How should companies comprehensively measure employee performance? How can the human factor be ensured to generate sustainable value?

This issue of CFO Express focuses on the above issues, and we hope that these excerpts and summaries will provide new insights and ideas for corporate decision-makers.

Chief Economist's View |

|

Trends and Outlook |

|

Expertise and Practice |

|

Talent and development |

Chief Economist's View

Chief Economist's View

Establishing the new before destroying the old

Deloitte China's Chief Economist, Sitao Xu, shares his perspectives on China's economic outlook of 2024. His main takeaways are:

- China's key economic goals for 2024 can be boiled down into three aspects: GDP growth, inflation, and projected deficit (the room for monetary easing is relatively constrained). We believe that the growth target of "around 5%" is feasible, but as the base effect becomes less favourable this year, it is not easy to reach this target.

- The economic data for the first two months of this year has been relatively positive, with inflation being subdued so far. If the trend of Q1 data persists, growth could rely more heavily on external demand. Due to the impact of U.S. tariffs, supply chain restructuring and intense domestic market competition, companies have shown a willingness to explore overseas market. The incentive for firms and consumers to trade in old appliances and machinery for new ones will help to expand domestic demand, but such a scheme is unlikely to alter the dynamics of overcapacities.

- Currently, China's export environment is facing protectionism risk, which has been intensifying among China's main trading partners. In the long run, protectionism in the external environment may drive Chinese companies to accelerate localization in the overseas market, but in the short run, this has raised the risk of another episode of a trade spat. In addition to protectionism, another external uncertainty comes from the Fed— a strong US economy has prompted the Fed to postpone their timetable of cutting interest rates, but strong dollar and high US interest rates are constraining the PBOC's potential to reduce rates.

More information: The Deloitte Research Monthly Outlook and Perspectives (Issue 89)

Trends and Outlook

Trends and Outlook

Interpretation of 2024 Government Work Report and Industry Outlook

2024 marks the 75th anniversary of the founding of the People's Republic of China and is a crucial year for achieving the goals and tasks in the 14th Five-Year Plan. The principle about economic work is refined by the central government in the "Government Work Report": seeking progress while maintaining stability, promoting stability through progress, and establishing the new before abolishing the old. Based on our mid-to-long-term observations of China's economy, we look at future policy priorities from both macro and industry perspectives, as well as development opportunities for industries and enterprises.

Figure: Overview of Government Work Targets for 2024

Indicator |

2023 Government Objectives |

2023 Actual Value |

2024 Government Objectives |

GDP Growth Rate |

Around 5% |

5.2% |

Around 5% |

Increase in CPI |

Around 3% |

0.2% |

Around 3% |

Energy consumption per unit of GDP |

Continue to decline |

- |

Decrease by about 2.5% |

New urban jobs |

About 12 million people |

12.44 million people |

More than 12 million people |

A surveyed urban unemployment rate |

Around 5.5% |

5.2% |

Around 5.5% |

Monetary policy |

Implement a prudent monetary policy in a targeted and forceful manner |

- |

Pursue a prudent monetary policy in a flexible and appropriate, precise and effective way |

M2 growth rate |

Match with nominal economic growth |

9.7% |

Aligned with the expected targets of economic growth and price levels |

Fiscal policy |

Pursue a proactive fiscal policy with greater intensity and enhance its performance |

- |

A proactive fiscal policy should be moderately strengthened to improve quality and performance |

Deficit Rate |

3% |

- |

3% |

Source: 2024 Government Work Report, Wind

This year's Government Work Report is concise and pragmatic, presenting a policy direction that emphasizes on both "growth stabilization" and "high-quality development".

The government has set this year's economic growth target at "around 5%", which is consistent with the target of 2023. As the base effect becomes less favorable this year, this target is overall positive, reflecting the general principle of "promoting stability through progress". The government also attaches great importance to employment and living standards, setting the target for new urban jobs at "more than 12 million", the highest value in recent years, and emphasizing "scale up support for industries and enterprises with large employment opportunities". This also means that the service industry and platform economy will be better leveraged in the role of providing employment.

Currently, the working logic of China's economic development is showing some obvious changes, with the growth model mainly driven by investment and exports reaching its limit. On the one hand, attention needs to be paid to the issue of inadequate return on infrastructure investment. On the other hand, it is important to focus on adverse factors that exports are facing, for example, the EU launching anti-subsidy investigation against electric vehicles imported from China, which may lead to punitive tariffs; in some countries, deindustrialization is resisted, while in some emerging markets, competition is discouraged. These factors mean that introducing strong stimulus policies like that of 2008 should be very cautious, as it may result in overcapacity that will be even more difficult to handle in the current protectionist environment.

In terms of macro policies, this year's report proposes that a proactive fiscal policy should be moderately intensified to improve efficiency. Starting this year, it also plans to issue ultra-long special treasury bonds in next several years. Building on last year's issuance of 1 trillion yuan of government bonds, the government has further expanded fiscal policy by showing that policymakers are determined to drive economic growth. Considering the current low level of inflation and the Federal Reserve's policy shift from tightening to easing, China still has ample space for policy implementation. At the National People's Congress press conference, Pan Gongsheng, the governor of the People's Bank of China stated at China still has room for rate reductions, planning to use a variety of monetary policy tools to step up countercyclical adjustments and maintain reasonable liquidity.

In terms of major tasks, the new development philosophy should continue to guide efforts, with a primary focus on accelerating the development of new productive forces, expanding domestic demand, stimulating the vitality of market entities, expanding high-level opening-up, and promoting green and low-carbon development to drive high-quality development.

Major government tasks in 2024

![]()

More information: Interpretation of 2024 Government Work Report and Industry Outlook (Chinese version only)

Q1 2024 Review and Outlook for Chinese Mainland & HK IPO markets

As of 31 March 2024, in terms of the IPO funds raised, New York Stock Exchange led the global ranking while Nasdaq came in 2nd. Switzerland's SIX Swiss Exchange and the National Stock Exchange of India took 3rd and 4th position respectively. The new listings of a handful of large manufacturing and technology, media and telecommunications companies enabled Shanghai Stock Exchange to earn 5th place in the ranking.

Following the announcement of several regulatory measures that heightened scrutiny of A-share listings and issuer quality, mainland IPO activity slowed further in Q1 2024. Compared to its performance over the last two years, overall A-share IPO market activity is forecast to slow considerably throughout 2024. In the long run, these regulatory measures will create a healthier market by setting a higher benchmark for listed companies, delivering enhanced benefits from the stock market to the overall economy and contributing more to economic growth.

The CMSG forecasts that the A-share IPO market will have around 115 to 155 new listings raising about RMB139 to RMB166 billion. All five markets will have fewer new listings this year: the main boards in Shanghai and Shenzhen are expected to have 25 to 35 IPOs raising RMB74 billion to RMB84 billion; ChiNext is forecast to have 35 to 45 new listings raising RMB30 billion to RMB37 billion; the SSE STAR Market is anticipated to have 20 to 25 IPOs raising RMB28 billion to RMB35 billion; Beijing Stock Exchange is likely to have another 35 to 50 new listings raising RMB7 billion to RMB10 billion. Hong Kong is expected to have 80 IPOs raising HKD100 billion in 2024.

Despite various anticipated economic stimuli from the Chinese mainland for high-quality economic development and different measures to improve the Hong Kong stock market turnover and competitiveness in the short, medium, and long term, the timetable of US interest rate cut in the next three quarters would be one of the key factors in directing the flow of the funds and determining the rebound of the Hong Kong IPO market in 2024. Companies that have filed for A-share listings may switch their listing plans to Hong Kong may become another potential trend. As the A-share IPO activity continued to slow down in Q1 2024, Chinese companies remained active in listing in the US. The US IPO market for Chinese companies is going to face similar fate as the Hong Kong market, i.e., more companies that planned to list in the Chinese mainland will divert their plans to the US instead in order to raise funds in a more timely manner. We expect most of the Chinese companies will complete their US listings before the US Presidential Election this year.

More information: Q1 2024 Review and Outlook for Chinese Mainland & HK IPO markets

Expertise and Practice

Expertise and Practice

The next set of imperatives for CFOs in the Asia-Pacific region, reveals Deloitte Survey

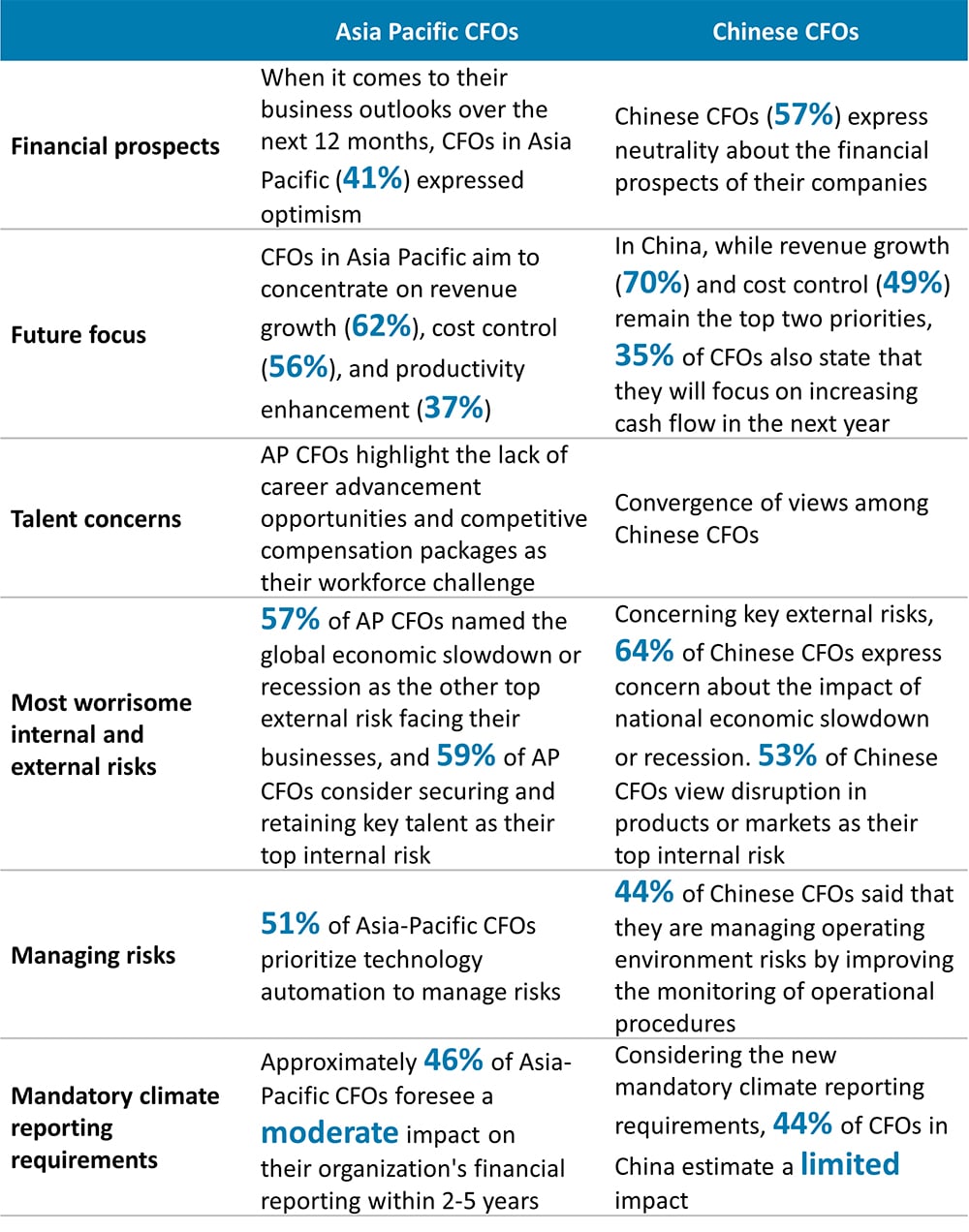

Currently, organizations in all regions of the world are having to navigate a landscape marked by economic fluctuations, slowing growth, surging inflation and an era of elevated interest rates. The survey was conducted across five economies in Asia-Pacific, namely, Australia, China, India, Japan, and SEA, we surveyed 276 CFOs in the region to better understand their challenges, priorities, and ways they are navigating the future. The report finds that, most Asia-Pacific CFOs are optimistic or neutral about the prospects of their national economies. In the face of challenging external and internal circumstances, traditional roles within the CFOs are metamorphosing to become broader, with boundaries between functions becoming more fluid. They become a key enabler for their organizations to achieve digital transformation and sustainable development.

Key findings from CFO surveys in China and Asia-Pacific Region

CFOs across Asia-Pacific were overall optimistic on the regional economic outlook. The key priorities for business across the Asia-Pacific region over the next 12 months are revenue growth (62%), cost control (56%), and productivity improvement (37%). And, in China revenue growth (70%) and cost control (49%) remain the top priority areas.

As the region's regulatory landscape is transitioning from voluntary to mandatory disclosures, companies are facing the urgent challenge for addressing the climate change imperative. Survey results show that more than half of CFOs (56%) are prepared for ESG-related matters. Changes in technology and regulation are affecting priorities in Asia Pacific, and achieving a deeper integration between finance, business, and technology is essential for evolution.

More information: The next set of imperatives for CFOs in the Asia-Pacific region

A guide to emerging technologies for CFOs

In recent years, artificial intelligence (AI) has great application potential in Finance, and some organizations have broadly used it to process self-service and enterprise resource planning (ERP). But skepticism also arises about the limits of generative AI, return on investment, and the new possibilities brought about by other emerging technologies. Deloitte published a report "Crunch time series: Novel and exponential technologies in Finance", focusing on analyzing the opportunities and challenges that emerging technologies bring to Finance and providing advice for financial leaders on ‘how to better leverage on emerging technologies such as AI capabilities in the future'.

The report reviewed classical scenarios in which AI, machine learning and generative AI can be applied to Finance. The automation logic of AI can help streamline financial processes for enterprises, such as invoice processing and account reconciliation; it can also provide a careful and intelligent risk assessment. Additionally, its document processing capability is also significant, automatedly extract and analyze information from financial documents such as invoices, purchase order and contracts. Machine learning, which emerged together with AI, assists enterprises establish intelligent supply chains, predict large volumes of data, and detect vulnerabilities. In terms of tax compliance, machine learning not only identify "holes" in data provided by other functions, but also potentially reduce the labor cost needed to reconcile data that the tax department needs for compliance and assessing risk. Generative AI can autonomously conduct scenario modeling, build intelligent avatars, and perform scenario monitoring. In the future, generative AI are expected to be utilized in many other potential scenarios, such as strategic finance, business unit finance, and operational finance.

The report also examines the potential benefits that may be brought about by emerging technologies, such as augmented reality, digital twin, and quantum computing. Deloitte believes that the development of these technologies can help organizations evaluate, design, and plan their financial decisions, and accurately identify their internal risks.

Deloitte believes that business leaders and financial decision-makers need to take measures in Finance, balance the topics of governance and control with regards to people, technology, and data, thus help companies more efficiently take advantage of emerging technologies. These measures include:

First, prepare your talent and organization for the work, coordinate goals, and learn skills related to emerging technology operation, to better adapt and apply those technology capabilities in the future.

Second, closely monitor the implementation of emerging technologies, and seize the moment to upgrade enterprise resource planning (ERP), to enhance agility and efficiency ahead of competitors.

Third, monitor and control the data sources used in emerging technologies, ensure their quality and safety, establish a complete and formal management and testing system, and support the development of technology with consideration of ethical principles.

Lastly, establish relevant measures to strengthen governance and control of emerging technologies, especially in the context of large-scale use of artificial intelligence. This will help to prevent potential cyber threats to businesses and ensure the safe and rapid development and application of technology.

More information: Crunch time series: Novel and exponential technologies in Finance (Chinese version only)

New frontiers of sustainability: Double Materiality explained

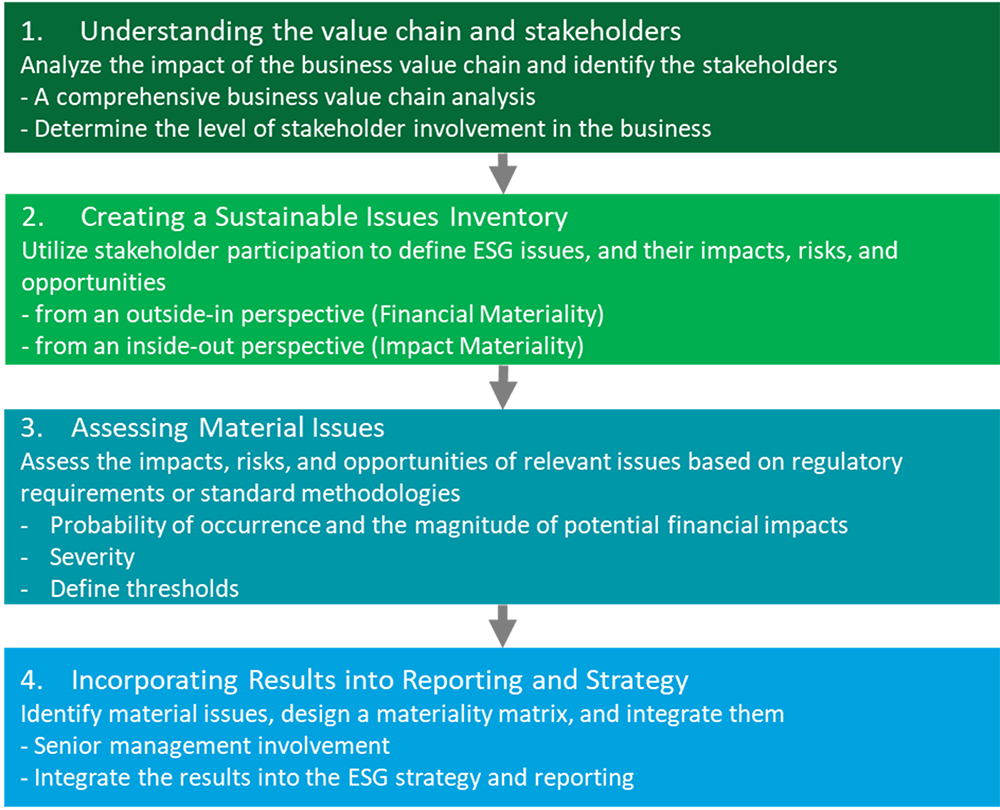

In February 2024, China's three major stock markets, the Shanghai Stock Exchange (SSE), the Shenzhen Stock Exchange (SZSE), and Beijing Stock Exchange (BSE) – released a draft guideline on sustainability Report (Provisional), which clearly introduced the concept of Double Materiality. The draft requires that the disclosing entity identify whether based on industry and business characteristics, each topic set out in this guideline has a significant impact on the enterprise value (referred to as "financial materiality"). The entity shall also evaluate whether the company's performance in corresponding topic will have a significant economic, societal, and environmental impact (referred to as “impact materiality”). In addition, the entity shall illustrate the process of analyzing sustainability topics by importance.

Materiality assessment serve as a starting point for determining the topics to be disclosed in the sustainability report, as well as the corresponding impacts, risks, and opportunities. Under Double Materiality, impact materiality refers to the significant impacts that business-related issues bring to the environment and society. The scope of this definition not only includes the direct impacts of the company, but also the impacts generated in the enterprises' value chain and other business relationships. Financial materiality primarily assesses risks or opportunities and refers to the significant impacts that business-related issues have on corporate management, financial situation, cash flow, and financing ability. Generally, "impact materiality" and "financial materiality" are interlinked. After a company identified the material topics, it should determine the information needed to be disclosed for each material topic based on the importance of information. The sustainability report is part of company's management report and should be released annually.

Double Materiality assessment in sustainability disclosure is a considerable challenge for many companies. It requires companies not only to examine the impacts of their business on environment and society, but also understand how these impacts, in turn, affect the company's finances and long-term sustainability. However, this challenge also indicates the important direction of future sustainability disclosure. With increasing global regulatory requirements and stakeholder expectations, preparations in advance and actively addressing Double Materiality assessment will become an indispensable part of corporate sustainable development strategy.

Step-by-step overview of Double Materiality assessment

More information: New frontiers of sustainability: Double Materiality explained (Chinese version only)

Talent and development

Talent and development

2024 Global Human Capital Trends: Embracing Human Sustainability

At the China Development Forum (CDF) 2024 Annual Meeting, Deloitte shared the "2024 Global Human Capital Trends" report, calling on business leaders to focus on trust and sustainable human development. The report identifies seven trends that showcase how a combination of business and human outcomes plays a role in organizational success. This year's analysis reveals that organizations making meaningful progress on these key issues are nearly twice as likely to achieve desired business and human outcomes.

Executives and employees are focusing on "human sustainability"

Prioritizing "human sustainability" means that organizations adhere people-centered principle to create value for employees, leaving them with greater well-being, employability, and equity. However, only 41% of employees believe that organizations have successfully done so. Workers identified increasing work stress and the threat of technology taking over jobs as the top challenges to organizations embracing human sustainability.

Redefining "human performance" with data and trust

In today's complex and changing work environment, traditional productivity metrics such as working hours and time-wasting on tasks are no longer sufficient to assess human performance. The advancements in technology and data collection have brought more effective metrics for organizations. With the increase in data, organizations increasingly need to establish transparent data practices to build trust among employees.

Employees need more organizational support as disruptions accelerate

The rapid development of artificial intelligence (AI) and generative AI highlights the importance of organizations support for employees to develop the sustainable competencies such as curiosity and empathy. Most respondents (73%) emphasized the importance of keeping human imagination in sync with technological innovation. To close the imagination deficit, organizations should encourage innovation through digital s — which give workers the psychological safety to explore intentionally, tapping into their capabilities as they experiment with new technologies.

Encouraging organizations to embrace more diverse "microcultures"

While upholding the organizational values, employee also wish to autonomously establish a unique microculture tailored to team's needs. The HR department should cultivate a pool of "talent expertise" across the entire organization to ensure right skills available for business development, rather than just functioning as an independent department.

More information: 2024 Global Human Capital Trends

Contact us

If you need any further information, please feel free to reach out to your Deloitte contact person, or reach out to us via the following contact details.

Norman Sze

Vice Chair

Deloitte China

Phone: +86 10 8512 5888

Email: normansze@deloitte.com.cn

Maggie Yang

Partner

Deloitte Consulting China

Phone: +86 10 8520 7822

Email: megyang@deloitte.com.cn

Michael Jin

Partner

Deloitte Consulting China

Phone: +86 21 2316 6317

Email: mijin@deloitte.com.cn

Bo Sun

Senior Manager

Deloitte China CXO Program

Phone: +86 10 8512 4866

Email: bsun@deloitte.com.cn

Explore Content

- Play this episode

- Establishing the new before destroying the old

- Interpretation of 2024 Government Work Report and Industry Outlook

- Q1 2024 Review and Outlook for Chinese Mainland & HK IPO markets

- The next set of imperatives for CFOs in the Asia-Pacific region, reveals Deloitte Survey

- A guide to emerging technologies for CFOs

- New frontiers of sustainability: Double Materiality explained

- 2024 Global Human Capital Trends: Embracing Human Sustainability